|

Tax & Accounting Issues in Korea’s Publishing Industry

2021.02.08

Recent trend in the Korean publishing market

Looking at the overall trend in the history of the Korean publishing market, paper books had been taking the center for a long time. However, e-books or the “e-book market” emerged, and today, publishers are having a greater interest in exporting copyrights of publications. This phenomenon has led to reduced demand for physical facilities, spurring the establishment of single-person publishers and small-sized publishing companies.

Tax structure related to publishing in Korea

The types of tax imposed on publishers running a business in Korea are as follows:

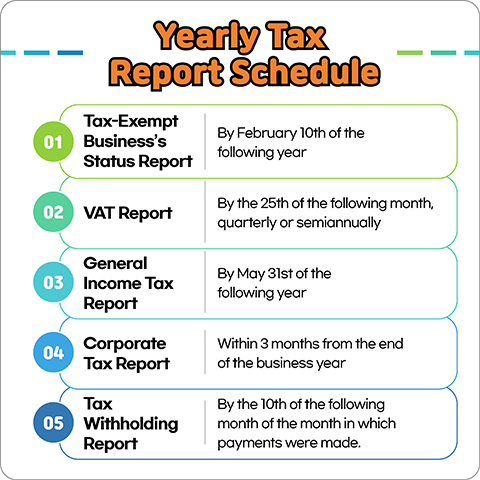

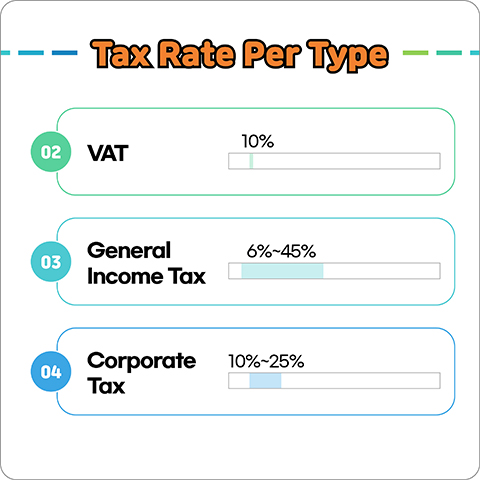

1. Value-Added Tax (VAT) Publishing companies are primarily VAT-exempt business entities. However, more publishers are expanding their business to selling products related to books or promoting educational programs on top of publishing books. If a publisher is engaged in both tax-free business and taxable business, it must be registered as a taxable business entity.

2. General Income Tax & Corporate Tax If an individual business or a corporate business has a certain level of income, it is subject to pay tax corresponding to the amount. To be specific, “corporate tax” is imposed on the income earned by corporate businesses such as an incorporated company, and individuals who make profits should report and pay “income tax.”

3. Tax Withholding (Monthly Wage, etc.) As a certain amount of tax is deducted from the monthly wage of company workers, the actual amount they get in their bank accounts differs from the notified total wage. Such pre-deduction of tax by companies is called “tax withholding.” Businesses are primarily obliged to withhold tax for earned income and social insurance fees such as the national pension from wages before paying their employees.

Tax Benefits for Publishers

There is an array of tax benefits that publishers running a business in Korea can enjoy. Representative tax credits are as below:

Tax Issues Related to Copyright Exports

Exporting copyrights of publications is indeed an exciting thing that yet not many have tried or are doing. However, it is quite different from traditional exports, and as it is affected by tax treaties and international taxation on top of the general tax law, it is easy for publishers to experience failure due to lack of knowledge.

Copyright export is attractive indeed, but considering its different nature compared to traditional exports, thorough understanding is a must.

The next keyword is “Tax Withholding Overseas.”

Written by Kim Hyun-Joon (Tax Accountant at Tax Consulting Firm With Plus)

Kim Hyun-Joon (Tax Accountant at Tax Consulting Firm With Plus) |

Pre Megazine

-

New Tarot Made With Korean Colors and Patterns!

VOL.69

2024.04 -

Please Look After Mom by Shin Kyung-sook

VOL.69

2024.04 -

Paper Play – A Great Way for Emotional Development, Concentration, and Creativity!

VOL.68

2024.03 -

Submit Us Your Reviews of Korean Books!

VOL.68

2024.03 -

A Miraculous Workout Routine for a Healthier Body!

VOL.67

2024.02 -

The Hottest Place in Korea, Right Here, Right Now!

VOL.66

2024.01 -

Kim Jiyoung, Born 1982 by Cho Nam-Joo

VOL.66

2024.01 -

Concerning My Daughter by Kim Hye-jin

VOL.65

2023.12 -

Bake Delicious Bread that’s Just Right for Your Taste

VOL.65

2023.12 -

Craft Your Own Special Miniature Furniture

VOL.64

2023.11 -

Take Beautiful Palace Tours With a Book

VOL.63

2023.10 -

A Guide to Beautiful Korean Handwriting

VOL.62

2023.09 -

An Offbeat Trip to Jeju Island

VOL.61

2023.08 -

Prepare for Disasters with a Single Book

VOL.60

2023.07 -

The Hen Who Dreamed She Could Fly by Hwang Sun-mi

VOL.60

2023.07 -

Feel the Street Vibes with Watercolor Painting

VOL.59

2023.06 -

Bone Soup by Kim Young-tak

VOL.59

2023.06 -

Eat Healthier and Tastier – Korean Vegan Food

VOL.58

2023.05 -

Almond by Won-pyung Sohn

VOL.58

2023.05 -

Learn About and Have Greater Fun Drinking Korean Alcohol!

VOL.57

2023.04 -

Knitting YouTuber Daeri Kim’s “Easy Modern Daily Knit”

VOL.56

2023.03 -

A New Section for Readers’ Reviews!

VOL.55

2023.02

Copyright© 2019 KIPIA. All Rights Reserved.